Black Box Ltd

About the Company

Black Box Ltd, founded in 1976, began as a provider of connectivity solutions such as cables and adapters, later evolving into a global leader in IT infrastructure and communication solutions. Known for its expertise in networking, data centers, and cybersecurity, the company expanded its reach during the 1980s and 1990s by integrating complex IT systems and establishing a strong global presence. In 2018, it was acquired by AGC Networks, part of the Essar Group, further enhancing its capabilities in digital transformation and advanced technologies like IoT, AI, and cloud computing. Today, Black Box Ltd is a trusted partner for secure IT solutions across industries worldwide. It is a global digital infrastructure integrator, delivering network and system integration services, support services, and technology products to businesses in the United States, Europe, India, Asia Pacific, the Middle East, and Latin America, employing around 4,000 professionals globally. Black Box offers robust services in network integration, digital connectivity infrastructure, data center build-outs, modern workplace solutions, and cybersecurity, serving industries such as financial services, technology, healthcare, retail, public services (including airports), manufacturing, and more.

Promoter insights:

Anshuman Ruia (Executive Director): A prominent leader within the Essar Group, Anshuman Ruia plays a crucial role in providing strategic direction to Black Box Limited. His association with the Essar Group brings extensive expertise in managing large-scale global businesses across infrastructure, technology, and industrial sectors.

Sanjeev Verma (Whole-Time Director): Sanjeev Verma oversees the operational and strategic execution of BBL's digital infrastructure business. Under his leadership, the company has undergone significant transformation, focusing on innovation, profitability, and customer-centric solutions.

Deepak Kumar Bansal (Executive Director & CFO): As the Global Chief Financial Officer, Deepak Bansal has been instrumental in maintaining financial discipline, achieving operational efficiencies, and driving profitability.

Business Overview

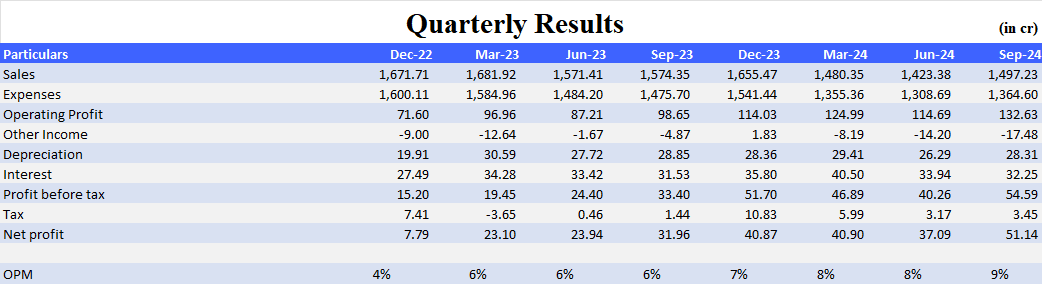

Financial Report

Share Capital & Number of Employees

Share price and Volume (last 1 year):

Month and Year |

|---|

| Volume |

Prev Close

N/A

Sector

IT - Software

Market Cap

₹8305 Cr.

TTM PE

N/A

Sectoral PE Range

N/A

PE Remark

N/A

BSE

N/A

COMPANY TYPE | EVERGREEN |

|---|

| (IN INR CR) |

|---|

| (IN INR CR) |

|---|

Key Metrics

Market Cap

₹8,305 Cr.

Current Price

₹494

PE Ratio

43.1

D/E Ratio

1.48

ROCE%

30.9%

CWIP

₹0 Cr.

ROIC%

N/A

Cash Conversion Cycle

-69 day

ROE%

42.5%

PEG Ratio

0.57

Business Segment

Consulting Business

Technology Product Solution

System Integration

Key Highlights & Management Guidance

Order Book:

• Total order booking stood at US $470 million as of March 2024 compared to US $490 million as of Dec 2023. Order Book Split:

1. Projects- 37%

2. Manage Services + T&M- ~31%

3. Maintenance Contract- ~29%

4. Products- ~3%

The co. focuses on large deals, in FY24, it bagged a $105 Mn deal for Data Center and In-Building 5G/OnGo solutions, a $21 Mn deal for On Demand and Connected Building solutions, and a few more deals worth $5 Mn+.

Acquisitions and Partnerships:

• Acquired cybersecurity and IoT companies in Australia, UAE, and India, enhancing its technology portfolio.

• Strategic partnerships with leading hyperscalers and cloud providers, supporting large-scale data center projects.

Capex and Expansion Plans:

• The company is intensifying its focus on data center infrastructure, fueled by increasing CAPEX investments from hyperscalers and cloud providers. With a project backlog of US$ 455 million as of September 2024, it anticipates strong growth in the data center segment, driven by the surging demand for digital infrastructure solutions.

Customer Base and Revenue Mix:

• Currently, 20% of revenues come from the data center segment, with expectations to increase this to 25-30% over the next few years.

• Gross margins for data center services are around 20%, while IT services margins are higher, between 27-29%.

Go-to-Market (GTM) Strategy:

The company has revamped its Go-to-Market (GTM) strategy by aligning with industry verticals and technology horizontals to strengthen its customer-centric approach. It aims to prioritize growth by focusing on its top 300 clients while making substantial investments in leadership talent and sales teams to enhance market penetration.

Industrial Outlook

Introduction

The Indian IT industry is a key driver of economic growth, innovation, and global digital transformation. With a skilled workforce, strong export demand, rapid digital adoption, and supportive government policies, the sector continues to expand its global footprint. As investments in AI, machine learning, and digital infrastructure increase, India remains a dominant force in the global IT landscape.

Indian IT Industry Market Size

India’s IT industry has seen remarkable growth, solidifying its position in the global technology market. According to NASSCOM, the industry’s revenue reached $227 billion in FY22, marking a 15.5% year-on-year (YoY) growth, and further expanded to $245 billion in FY23.

Key Market Insights:

IT Spending: Projected to grow 11.1% in 2024, reaching $138.6 billion from $124.7 billion in 2023, driven by investments in infrastructure, digital transformation, and emerging technologies.

Software Industry Growth: The Indian software product industry is expected to reach $100 billion by 2025, fueled by global expansion and enhanced delivery centers.

Data Annotation Market: Valued at $250 million in FY20, with the US contributing 60% of the market. It is expected to grow exponentially to $7 billion by 2030 due to rising AI adoption.

Projected Industry Revenue: The Indian IT sector is on track to reach $350 billion by 2026, contributing 10% of the GDP. IT exports grew 9% in constant currency terms to $194 billion in FY23.

Growth Drivers of the Indian IT Industry

1. Diverse End-User Market & Skilled Workforce

The demand for IT services extends beyond traditional tech companies to industries such as pharmaceuticals, retail, and utilities. Large organizations increased IT spending by 14% in 2015, indicating a broadening customer base. Additionally, India’s vast pool of technically skilled professionals continues to drive sector growth.

2. Digital Transformation

India’s digital ecosystem is expanding rapidly, supported by initiatives like Digital India and technological innovations such as Unified Payments Interface (UPI). UPI processes nearly 10 billion monthly transactions, accounting for 45% of global real-time payments. The increase in digital transactions from 300 crore in 2019 to 1,052 crore in 2023 highlights the nation’s digital progress.

With 850 million internet users and some of the lowest data costs globally, digital transformation has driven sectors like fintech, e-commerce, and government services.

3. Strong IT Export Demand

India’s IT and BPM exports have grown 14% annually over the past two decades, reaching $254.5 billion in 2021-22. IT services alone contributed $157 billion, employing 5 million people globally. The international demand for Indian IT talent continues to propel growth, reinforcing India’s position as a global technology leader.

4. Breakthroughs in AI & Machine Learning

The Indian technology industry recorded $227 billion in revenue in 2022, driven by advancements in AI, IoT, big data, cybersecurity, and robotics. The Indian AI market is projected to grow 20% annually over the next five years, making it the world’s second-fastest-growing AI market.

AI applications in banking, finance, fraud detection, and cybersecurity continue to expand, fueling IT sector growth. Government initiatives like the Digital India program are allocating $477 million to further AI-driven innovations.

SWOT Analysis of India’s IT & BPM Sector

Strengths:

Consistent Growth: Revenue reached $227 billion in FY22, projected to hit $350 billion by 2026.

Skilled Workforce: India has a vast pool of technical talent.

Cost Advantage: Lower operational costs make India a preferred outsourcing destination.

Weaknesses:

Dependence on Global Markets: Heavy reliance on the US and Europe.

Shortage of Skilled Talent in Emerging Tech: Gaps in AI, machine learning, and cybersecurity expertise.

Infrastructure Limitations: Some regions lack advanced IT infrastructure.

Opportunities:

Expansion in Digital Services: Growing cloud computing, AI, and cybersecurity adoption.

Automation & AI Growth: Increasing use of AI across industries.

Government Support: Policies and incentives boost technology adoption.

Threats:

Intense Global Competition: Countries like China and the Philippines offer competitive IT services.

Regulatory Challenges: Data privacy and security regulations impact compliance costs.

Geopolitical Risks: Trade disputes and conflicts can affect IT exports.

Government Initiatives Supporting IT Growth

Union Budget 2025-26: Government allocates ₹95,298 crore to Telecom & IT sectors.

IndiaAI Mission: Cabinet approved ₹10,300 crore (~$1.2 billion) to enhance AI ecosystems.

PLI Scheme 2.0: ₹17,000 crore (~$2.06 billion) allocated for IT hardware manufacturing.

Focus on Emerging Tech: Investments in cybersecurity, blockchain, and hyper-scale computing.

Future Outlook:

India remains a global leader in IT services and outsourcing, with substantial opportunities in emerging technologies. The IT sector’s revenue is forecasted to reach $350 billion by 2026, contributing 10% to India’s GDP.

Financial Highlights

| PARTICULARS | Q1FY24 | Q1FY25 |

|---|---|---|

| Sales | ₹6,288 Cr | - |

| Sales | - | ₹6,282 Cr |

| OPM% | 4% | 7% |

| EBITDA | ₹248 Cr | ₹412 Cr |

| Net Sales | ₹24 Cr | ₹138 Cr |

Shareholding Pattern

Mar'2024 | Jun'2024 | |

|---|---|---|

| Retailers | 71.09% | 71.06% |

| FIIs | 4.81% | 4.71% |

| DIIs | 0.01% | 0.01% |

Capsule’s View

1. Financial Growth Targets

Revenue Growth:

The company has projected revenue growth of 5-10% for FY25, driven by:

- Expansion in hyperscale data centers.

- Increased demand for connectivity and enterprise networking solutions.

- Greater adoption of cloud-based services and cybersecurity solutions.

Medium-term target: Achieve a revenue milestone of $2 billion by FY28, reflecting strong demand across geographies and industries.

Profitability and Margins:

EBITDA Margins:

- Targeted to stabilize at 8.1% in FY25, with continued cost optimization and improved pricing strategies.

- The focus is on achieving a sustainable margin improvement through:

a) Operational efficiency.

b) Better subcontractor management and facility optimization.

2. Market Drivers and Industry Trends

Digital Transformation:

- High demand for AI, IoT, and cloud solutions across industries is expected to drive growth.

- Increased investment in cybersecurity due to rising cyber threats.

Hyperscale Data Centers:

- Significant investments in hyperscale data centers to support hyperscalers, large enterprises, and multi-tenant operators.

- This segment is expected to grow exponentially over the next 3-5 years.

Connectivity Infrastructure:

- Focused investments in advanced networking, including 5G and edge computing, to meet the growing data demands of enterprises.

Challenges:

- Delayed project execution due to hold-ups in decision-making processes impacting revenue growth.

- Management noted that the decision-making delays stem from high interest rates and supply chain issues, particularly in the data center sector.